Break Even Analysis is one of the most popular and effective tools of cost volume and profit analysis. By using this we can calculate production quantity/sales quantity and their values whether there is a situation of neither profit nor loss. Apparel Industry is growing in India, Bangladesh, Vietnam, and the future of the apparel industry is very much competitive and challenging. Every year new modern garments factories are establishing to produce different garments to meet the worldwide increased demand for apparel. Here in this article, you will learn why break even analysis of apparel industry is required. Break-even point can be calculated for your whole factory, individual machine, equipment, production floor or any other investment opportunities. You can identify both forecasted BEP and actual BEP as required.

Break Even Analysis of Apparel Industry

As an investor, you must be careful about making an investment decision. The main concern should be the minimization of the production cost of garments and increasing the production of garments. Different project appraisal techniques like; cost-benefit analysis, break-even analysis, capital budgeting, etc. are used by the entrepreneur or manager to make the right financial decision. Normally the company is not aware of the break-even point if it is running a profit. But in the case of losing concern, the company must try to avoid loss situation to ensure the survival of the company. Break-even point analysis is also known as BEP analysis.

Calculation Break Even Point and Analysis of Apparel Industry

To calculate breakeven quantity or value, you will be required to have the following information:

- Sales Price Per Unit

- Total Sales Quantity/ Expected Sales Quantity

- Variable Cost Per Unit

- Total Fixed Cost

If you have a total sales amount and quantity of sales, then you can easily get the average per-unit sales price by dividing the sales amount with the sales quantity. Another thing is if your company produce many varieties of products and there is a far difference in price then it will be good for you to choose a weighted average sales price instead of calculating average sales price.

On the other hand, the variable cost per unit is the amount of cost which remains fixed for any level of production or sourcing.

For your better understanding, I am giving a simple example of break-even analysis in details.

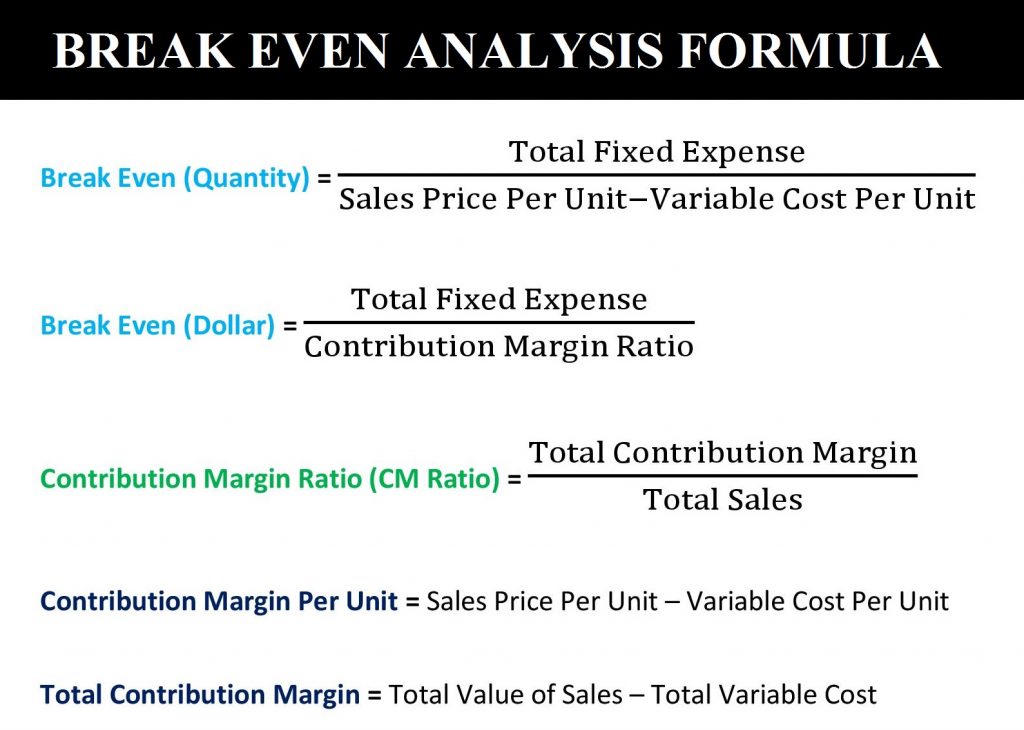

Break-Even Analysis Equation or Formula

Two basic formulas of break-even analysis are most popular, one is used for calculating the break-even quantity and another one is for break-even values.

Break Even (Quantity) = (Total Fixed Expense)/(Sales Price Per Unit-Variable Cost Per Unit)

Contribution Margin Per Unit = Sales Price Per Unit – Variable Cost Per Unit

Total Contribution Margin = Total Value of Sales – Total Variable Cost

Break Even (Dollar) = (Total Fixed Expense)/(Contribution Margin Ratio)

Contribution Margin Ratio (CM Ratio) = (Total Contribution Margin)/(Total Sales)

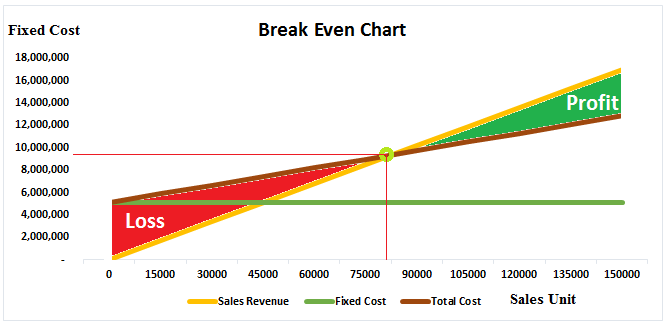

Break Even Analysis Example

In this break-even graph, you can see that with the increase in sales volume fixed cost remains the same for a particular period but the total cost is increasing. Total cost includes fixed cost and variable cost. Only increase of variable cost is there with the increased in production or sales. Here the thing is when you increase the sales, per unit fixed cost, will be reduced but total fixed cost remains the same. Fixed cost is shown by the straight horizontal line in the graph. On the other hand per unit variable cost will remain unchanged but the total variable cost will increase. So there is a relationship between cost, sales quantity, break-even unit, and profitability.

Calculation of Break-Even Point

Suppose you are the manufacturer of T-shirt. You want to calculate break-even quantity and value (USD) for a particular year. So that you can determine your minimum requirement of production to run your factory at profit. Based on the following information when you put the values in the above formulas you will get the value of break-even point.

- Sales Price Per Piece: 1.6 USD

- Variable Cost Per Piece: 1.01 USD

- Total Fixed Cost: 500,000 USD

- Sales (Quantity): 1,000,000 Piece

- Total Sales: 1,600,000 USD

- Contribution Margin Per Unit: 0.59 USD

- Total Contribution Margin: 590,000 USD

- Contribution Margin Ratio: 0.37

- Break Even (Quantity): 847,458 Piece

- Break Even (Value): 1,355,932 USD

Here, the break-even quantity is 847,458 piece, this means you have to produce this number of the T-shirt to remain a situation where there is no profit and loss. On the other hand, you need to sale total of 1,355,932 USD. If you can sell more than this then you will get profit. That is in addition to your break-even there will be an addition to your profit amount. So this is an easy way to set the target of your factory.

Break-Even Analysis Excel Template

I have developed a simple break-even analysis excel template for your better understanding and which is available for free use. You can use the excel template as a break-even calculator. All you need to input the values of cost and sales. If you want to get this then please comment with your email.

Calculate Garments Break-Even Production

There is no such difference among the BEP calculation and analysis of the different industry. The same methodology is applicable to the apparel industry and others. So to calculate garments break-even unit or value, same formula mentioned above you can use. All you need to gather information on your garments annual fixed cost, weighted average sales price and per unit variable cost. If you do not know how to calculate the weighted average cost then please let me know. I will write a detailed article on it.

Garments Break-Even Analysis

Analysis of Garments BEP is obvious for new garments industry or running company which is finding it hard to make a profit or incurring losses. Whatever result you will get from the calculation to find out the BEP unit or the amount you can decide what should be your target. Moreover, this will help to make the right economic decision for your factory. If you have any question regarding break-even point analysis of apparel industry then please contact with me. I can help you to calculate break-even for your whole factory, parts of the factory, machine or a production floor.

Written by

Md. Nahian Mahmud Shaikat

Hello Md. Nahian Mahmud Shaikat!

Thanks for sharing your article. We are interested in furthering discussion with regards to the factory which we are working on deploying.

It will be a great pleasure to have you on board. Thanks again and Remain Blessed!!!

I. b Inyang

Ebony Sports / Yali Yali Sportswear

Thank you for your comment. It would be our pleasure to work with you.

Hi Mr. Nahian Mahmud Shaikat,

It was a wonderful article about BEP in textile industry. Can you share the excel format for calculation of BEP.

Thanks in advance.

B/Regards

Ajay Singh

Hey I need break even analysis for apperal industry,could you pls help me to get it,also I need consumption calculation sheet.

Please contact through email at [email protected]

Hi i need the BEP calc sheet for my school project, my email is [email protected]. this was a helpful article.

Please send :)

[email protected]

Please send the excel file in the mail address [email protected]

It’s wonderful.. Can I plz get the excel file format of break even analysis.. My email Address is : [email protected].

Thanks,

shoeb

I need break Even Analysis report for garment industry,could you help to get Excel format.My Email address [email protected]

Tremendous resource for learning BEP analysis. Thanks for sharing the knowledge.

Good work – very helpful for non ie background.

welldone.

Thx/rgds

vijay

Very nice and informative article. Please email me the excel BEP

[email protected]

Very interesting article. Please send your excel sheet to: [email protected]

Thanks a lot.

CVP template

Dear Mr. Nahian Mahmud Shaikat

Appreciate your good work.

I would like to use this for our upcoming work.

So would you pls share me the excel file to review.

Waiting for your kind response.

With regards

Monir

hi please email me the excel sheet [email protected]

Very nice and informative article. Please email me the excel BEP

In this mail. [email protected]

[email protected]

Please email me the template

hi, please email the excel sheet. email is [email protected]

Hi I love to get also a copy of your excel template of these breakeven analysis. Thank you

Hi please email me the template…. thanks

Very interesting article.

can you Please Email me with excel sheet to: [email protected]

Thanks a lot.

I need break even point calculate excel template. please send me this email.

[email protected]