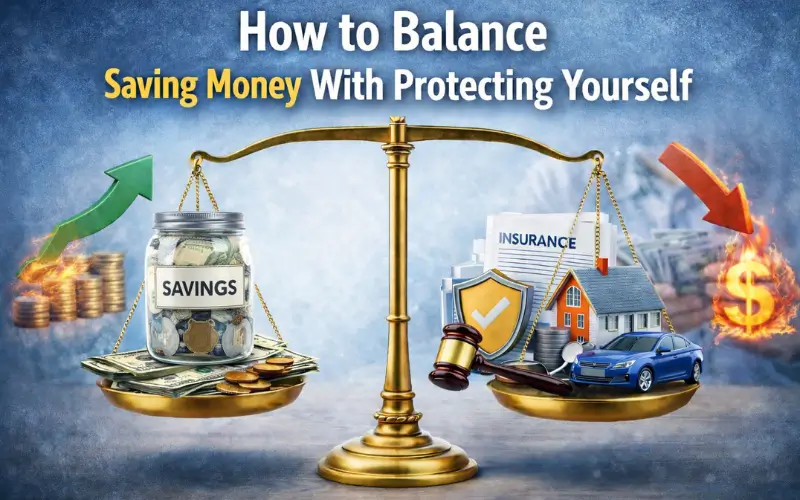

Money saving is usually considered the final personal finance objective, whereas protection is taken as a bothersome and required cost. As a matter of fact, these priorities are closely interrelated. Proper financial stability lies in striking the balance right between holding on to more of your earnings in the present and protecting yourself against expenses that might destroy your future. Knowing the saving and protection interactions enable you to make decisions that will propel you both in the short term and long term security.

Balancing Savings and Security

Most individuals are so much concerned with eliminating costs and not thinking about what they are risking. The temptation to omit protection or settle on the lowest possible price may feel like saving money but it tends to expose one to huge costs which are not predictable. A single accident, sickness or a lawsuit can nullify years of savings. The first thing in financial balance is the awareness that not all expenses are optional when you are aiming at securing what you have already established.

Meanwhile, protection does not imply spending without thinking. Spending more on a coverage that is not proportional to your condition can halt the goal-making towards other things such as saving an emergency fund or paying off debt. The trick is that it is possible to consider protection a financial tool but not a sunk cost. Coverage selected in a wise manner operates in the background as your savings will be spared unnecessary interruptions.

Evaluating Essential Protection

The financial weight of risks is not equal and this is why it is important to prioritize. Begin by listing those things that would inflict the greatest harm on your budget in case they happened. Transport is a leading weakness to a number of households. The accidents may cause expenses in repair of the accident, liability and disruption of income. That is why the decisions concerning auto insurance Ontario should not be renewed automatically or randomly.

It is also important when you evaluate essential protection to know what you are actually paying. Both value and cost are influenced by deductibles, coverage limits and optional add ons. Raising a deductible can also reduce monthly payments, although only when you are just comfortable enough to pay it. It is not aimed at eradicating risk but to ensure that you retain risk that you are able to manage without it straining your finances.

Periodically Going Over the Coverage

There is a fluctuation of financial situations and protection ought to vary with the situations. The amount of coverage that you require could be influenced by income increase, changes of lifestyle and large purchases. Something that was a sensible policy five years ago might not be the same policy that would fit your current priorities. Periodic reviews can encourage you to make sure you are either paying more or less than the current coverage or insurance cover that has gained more significance.

The same strategy can be used in case of housing risks. Home is your biggest asset in most cases and the price of underinsuring is also drastic. Periodic review of home insurance Ontario enables you to modify insurance cover as the price of houses, renovation expenses and personal conditions change. Through the balance between protection and your present financial status, you are able to save more assuredly knowing that the most significant risks are contained.

Striking a balance between saving and insuring is not about the extremes but rather about the motive. By taking conscious decisions that capture your ambitions and your risks, you create a financial base that becomes robust, adaptable and long-term.