In garment manufacturing, the terms SAM (Standard Allowed Minutes) and SMV (Standard Minute Value) are often used interchangeably.

But here’s the problem:

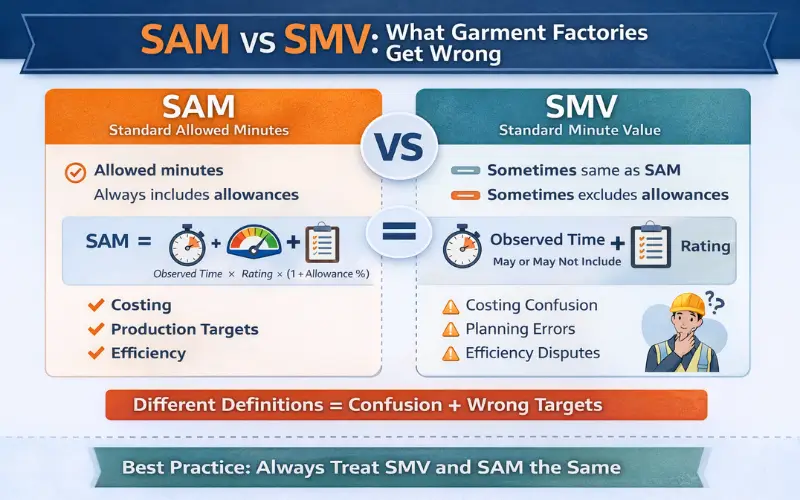

Many factories think they are the same — while calculating them differently.

That misunderstanding leads to:

- Wrong costing

- Unrealistic production targets

- Incorrect efficiency reporting

- Disputes between IE and production

- Buyer negotiation confusion

This article explains the real difference between SAM and SMV, where factories make mistakes, and how to standardize your system correctly.

What is SAM?

SAM (Standard Allowed Minutes): The allowed time in minutes for a trained operator to complete an operation at a normal pace, including allowances.

SAM always includes:

- Performance rating adjustment

- Allowances (fatigue, personal, delays)

SAM Formula

SAM=Observed Time × Rating Factor × (1+AllowanceSAM = Observed Time × Rating Factor × (1 + Allowance%) SAM= Observed Time × Rating Factor × (1+Allowance)

SAM is aligned with standard time principles in industrial engineering.

What is SMV?

SMV (Standard Minute Value) is widely used in the garment industry and often refers to:

The time required to produce a garment or operation.

However — and this is where confusion starts — SMV is used in two different ways in factories:

SMV = Same as SAM (Most Common in Garments)

Many factories use SMV and SAM interchangeably.

SMV = Only Normal Time (No Allowances Included)

Some factories calculate SMV without adding allowances.

That’s where planning errors begin.

The Core Difference Between SAM and SMV (In Practice)

| Factor | SAM | SMV (Common Use) |

| Includes Rating | Yes | Yes |

| Includes Allowances | Yes | Sometimes |

| Used for Efficiency | Yes | Yes |

| Used for Costing | Yes | Yes |

| Industry Terminology | IE standard term | Garment industry term |

The truth:

In many garment factories, SAM = SMV.

But in some cases:

SMV ≠ SAM

Because allowances are missing.

What Factories Get Wrong

❌ Mistake 1: Using SMV Without Allowances

If SMV excludes allowances, but production targets are set assuming full SAM, operators will never reach the target.

Result:

- Artificially low efficiency

- Frustrated production team

- Incentive disputes

❌ Mistake 2: Different Departments Using Different Definitions

IE department:

SMV includes allowances.

Production department:

SMV means raw sewing time.

Merchandising:

SMV is used for costing.

Without a unified definition, reports become inconsistent.

❌ Mistake 3: Buyers and Vendors Using Different Terms

Sometimes buyers say:

“Send garment SMV.”

But they assume it includes allowances.

If your factory sends normal time without allowances, costing becomes wrong.

❌ Mistake 4: Copy-Paste SMV From Previous Styles

Fabric changes

Machine attachments change

Seam type changes

But SMV stays the same.

That leads to inaccurate line planning.

Why This Confusion Is Dangerous

Let’s look at a simple example.

Observed Time = 0.50 min

Rating = 100%

Allowance = 15%

Normal Time = 0.50

SAM = 0.50 × 1.15 = 0.575

If factory uses:

SMV = 0.50 (no allowance)

But planning assumes:

SMV = 0.575

Then:

Target UPH (using 0.50) = 120 pcs

Realistic UPH (using 0.575) = 104 pcs

That’s a huge planning gap.

Efficiency Distortion Example

Efficiency formula: Efficiency = Produced SAM/Available Time

If SMV excludes allowances:

Efficiency looks artificially low.

Operators may appear inefficient — even when they are performing normally.

How to Standardize SAM and SMV in Your Factory

Step 1: Decide Your Definition

Choose one clear policy:

Option A:

SMV = SAM (includes allowances)

Option B:

SMV = Normal time

SAM = Normal time + Allowance

But never mix the two.

Step 2: Document Allowance Policy

Define:

- Base allowance %

- Special condition allowance

- Approval process

No guessing per style.

Step 3: Align All Departments

- IE

- Production

- Planning

- Merchandising

- Costing

Everyone must use the same definition.

Step 4: Update Operation Bulletin (OB) Format

Your OB should clearly show:

- Observed time

- Rating

- Normal time

- Allowance %

- Final SAM/SMV

Transparency removes disputes.

When Should You Use SAM vs SMV?

Use SAM when:

- Setting production targets

- Calculating efficiency

- Planning capacity

- Designing incentive systems

Use SMV when:

- Communicating with buyers

- Quoting garment minute values

- Internal costing references

But clearly define whether allowances are included.

Best Practice Recommendation

For garment factories:

Treat SMV and SAM as the same — and always include allowances.

This prevents confusion across teams and external stakeholders.

Final Takeaway

The problem is not SAM vs SMV.

The problem is unclear definition.

When factories:

- Skip allowances

- Mix terminology

- Copy old standards

- Fail to align departments

They create inefficiency without realizing it.

Standardize your definition, document your method, and validate on the floor.

That’s how you eliminate 90% of SAM/SMV disputes.