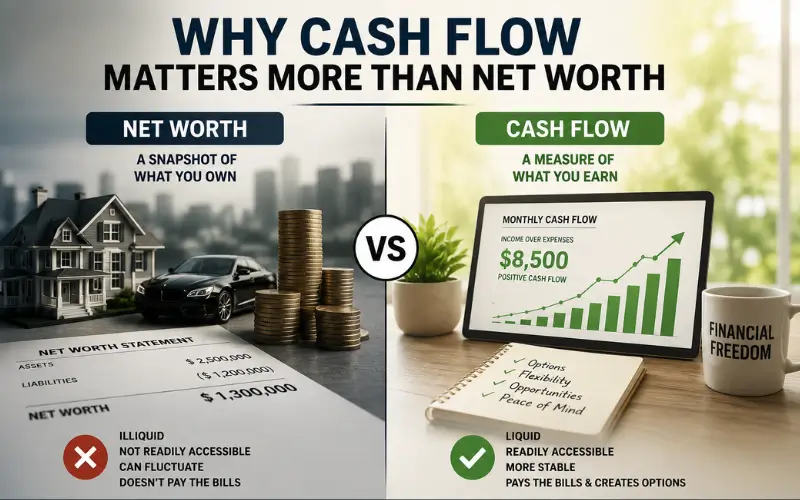

Ask most people how they measure financial success and they’ll point to net worth. It’s the number that gets cited in magazine profiles of wealthy individuals, the figure used to rank the richest people in the world, and the metric financial advisors often use to benchmark progress over time. Net worth has the appeal of being comprehensive: it takes everything you own, subtracts everything you owe, and arrives at a single number that supposedly tells the story of where you stand.

The problem is that net worth is a snapshot. It tells you what things are worth on paper at a particular moment. It says nothing about whether you can pay your bills next month, fund a business opportunity next quarter, or sustain your lifestyle if your primary income disappeared tomorrow. For those answers, you need to look at cash flow, and for most people in most circumstances, cash flow is the more honest and more useful measure of financial health.

The Difference Between Looking Wealthy and Being Financially Stable

It is entirely possible to have a high net worth and terrible cash flow. A business owner with a company valued at several million dollars but razor-thin operating margins, significant debt service obligations, and unpredictable revenue cycles may look wealthy on paper while experiencing genuine financial stress month to month. A homeowner who bought real estate at the right time may have substantial equity but no liquid income-generating assets and a fixed salary that barely covers their expenses. Net worth captures the former situation and misses the latter entirely.

The reverse is equally true. Someone with modest assets but reliable, diversified income streams — a rental property that cash flows positively, a business that generates consistent monthly revenue, dividend income from a well-funded investment account — may have a lower net worth than their peers but substantially more financial freedom in practical terms. They have options. They can weather a disruption. They can act when an opportunity appears.

Cash flow is what makes financial options real. Net worth, especially when it is tied up in illiquid assets, can feel more like a number on a spreadsheet than a resource you can actually use.

Why Cash Flow Banking Has Grown in Appeal

The concept of cash flow banking has gained significant traction among entrepreneurs, investors, and financially independent thinkers who have grown skeptical of the standard wealth-building prescription. The traditional model, maximize contributions to tax-deferred retirement accounts, wait thirty years, retire on the accumulated balance, asks people to lock capital away and defer access to it for decades. That approach may work for some, but it does nothing for the business owner who needs liquidity today, the investor who wants to move quickly on an opportunity, or anyone who experiences a financial disruption before the designated retirement age.

Cash flow banking, by contrast, emphasizes building systems that generate usable income now while still accumulating long-term value. Whole life insurance structured for the Infinite Banking Concept is one expression of this philosophy: premiums build cash value that remains accessible at any time without penalties, while the policy continues growing and eventually pays a death benefit. Rental real estate is another: a well-chosen property generates monthly income from day one while the underlying asset appreciates over time. The unifying principle is that money should work in ways that produce accessible, recurring cash flow rather than sitting locked behind age restrictions, market timing, or illiquidity.

Net Worth Can Evaporate. Cash Flow Is More Resilient.

The 2008 financial crisis illustrated this distinction with painful clarity. Homeowners who had built substantial net worth through real estate appreciation watched that net worth collapse as property values fell sharply. Because so much of their wealth was concentrated in a single illiquid asset, they had no buffer. People who lost jobs found themselves unable to service debt on homes worth less than they owed. Net worth, which had looked so solid on paper, turned out to be fragile.

Investors with diversified cash-flowing assets fared differently. Landlords with properly financed rental properties continued collecting rent throughout the downturn. Business owners with multiple income streams had options when one stream faltered. The cash flow kept coming regardless of what the underlying asset valuations were doing. It did not eliminate hardship, but it provided a degree of stability that paper net worth could not.

Market downturns, job losses, health crises, and economic disruptions are not rare exceptions. They are recurring features of any financial life played out over decades. A financial strategy built primarily around accumulating net worth through appreciating assets is more vulnerable to these events than one built around generating durable, recurring cash flow.

The Liquidity Problem With Net Worth

Even setting aside market risk, net worth has a practical limitation that rarely gets discussed: much of it is not readily accessible. Home equity requires either a sale or a loan to access. Retirement account balances come with early withdrawal penalties and tax implications. Business equity is illiquid until the business is sold or a financing event occurs. Private investment holdings may have no market at all until a specific exit event.

This means the net worth figure that looks impressive on paper may represent resources that cannot realistically be deployed when they are needed most. Financial emergencies do not wait for convenient exit opportunities. Business investments do not pause while you arrange a home equity line. The gap between what you own on paper and what you can actually access and use is wider for most people than they realize.

Cash flow does not have this problem. Income that arrives monthly is immediately deployable. A business that generates consistent revenue provides options that a business with unrealized appreciation cannot. Rental income funds expenses, investments, and opportunities without requiring any liquidation event. The practical usability of cash flow is part of what makes it a more reliable foundation for financial decision-making than net worth.

How Shifting the Focus Changes Financial Decisions

When cash flow becomes the primary metric rather than net worth, financial decisions start to look different. The question shifts from “how much is this worth?” to “what does this produce?” That reframe has significant practical consequences.

A real estate investor focused on net worth may chase appreciation in hot markets, buying properties that cash flow poorly or not at all, betting on continued price increases. A cash flow-focused investor evaluates every property by whether the rental income exceeds the carrying costs, and moves on quickly from anything that doesn’t meet that threshold regardless of how exciting the appreciation story sounds.

A business owner focused on net worth may reinvest everything into growing the company’s valuation while drawing a minimal salary, creating a situation where most of their wealth is concentrated in a single illiquid asset. A cash flow-focused owner thinks carefully about distributions, ensuring that the business funds a lifestyle and investment activity outside the company, which reduces concentration risk and creates financial stability independent of the company’s eventual sale.

These are not just different investment styles. They reflect a fundamentally different theory of what financial security actually means.

Building Toward Both, Starting With Cash Flow

None of this is an argument against building net worth. Long-term wealth accumulation matters, and assets that appreciate over time contribute meaningfully to financial security across a lifetime. The point is not to ignore net worth but to stop treating it as the primary goal while cash flow gets treated as secondary.

For most people in most financial situations, the more honest sequence is to build cash flow first. Establish income streams that cover expenses and generate surplus. Use that surplus to acquire assets that produce additional cash flow. Let the asset base grow over time as a byproduct of that process rather than as the target itself.

When cash flow is healthy, net worth tends to follow. When net worth is the only focus, cash flow often gets neglected until a disruption makes its absence impossible to ignore. The financial habits that produce lasting stability tend to start with the question of what a given dollar produces each month, not what it might be worth someday.

That shift in emphasis is small in theory and significant in practice.