Getting into a car accident is scary. Your heart races. Your mind goes blank. Even a small crash can feel Continue Reading

What Buyers Should Look for in Coastal Real Estate Investments

Investing in coastal real estate can be both exciting and rewarding. Investors find that with the right property choice, they Continue Reading

Learn From The Double Top: A 2025 Guide To Smarter Business-To-Finance Decisions

The double top pattern — feared by some, and often misunderstood — still carries weight in 2025. Despite algorithmic advancements Continue Reading

Explore Profitable Business Ideas with Minimum Investment

Do you know that initiating business does not need to be overly expensive? As online trading companies such as Flipkart Continue Reading

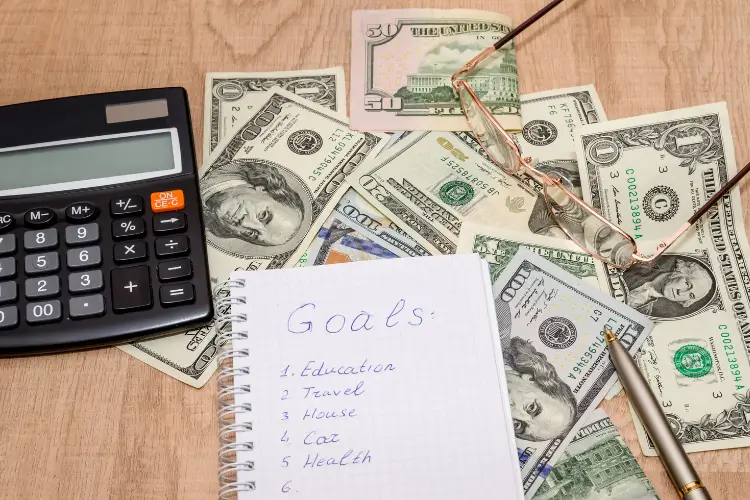

How to Achieve Your Financial Goals in 2025

Imagine a future where financial freedom is yours, dreams realized, and goals attained. Through careful planning and a solid approach, Continue Reading

Exploring the Different Types of Retirement Plans for Financial Security

Retirement is a stage of the life cycle where you no longer work, but the everyday reality of managing your Continue Reading